Pushing Back: Inside the Issue

Pity the airlines of South America. So many bankruptcies and near bankruptcies. Must be an awful market.

Au contraire. South America’s Big Four—or Big Three if you count Gol and Avianca as one—are earning some of their best operating profit margins ever right now. What in the world is going on? Our feature story this week explains.

No explanation is needed for why IAG continues to produce world-class profit margins. It’s pretty simple: Heavy exposure to the booming transatlantic market, and to Spain’s on-trend tourism sector. Air France-KLM is a structurally less profitable airline, with a disturbing downward earnings trend at KLM. But Air France has improved since the pandemic, and the low-cost carrier Transavia has big plans to boost its fortunes.

Across the group, big fleet changes are underway. Domestic French losses are in management’s crosshairs. Loyalty profits are a top priority. And so is consolidation, with SAS now firmly in its grasp, TAP firmly in its sights, and perhaps Air Europa firmly in its interests if IAG’s planned purchase meets the regulator’s axe.

Volaris is among the many Airbus Neo operators trimming capacity due to GTF engine woes. It managed to secure some compensation from Pratt & Whitney, which helped buttress the airline’s Q4 earnings. Still, it posted disappointingly low profits for all of 2023.

Not as disappointing as Norse Atlantic’s heavy losses though—losses that have some concerned about the airline’s long-term survival; a new Norse charter deal with Nigeria’s Air Peace suggests weakness, not strength.

No such concerns about Ryanair, but the Irish carrier itself expressed renewed concern about the pace of Boeing’s Max deliveries. As Air France-KLM made clear last week, there’s plenty of demand in the airline business right now. But it’s often difficult for carriers to get enough planes.

Before we get stuck into the meat of the issue, a quick invitation to share your thoughts and opinions with us. As we enter Airline Weekly’s 20th year, we’re keeping an open mind about new ideas and ways to make the edition even more enjoyable. If you’ve something to share, good, bad or somewhere in between, drop Gordon an email via [email protected]

The Airline Weekly Lounge Podcast

Gordon Smith and Jay Shabat examine the latest results from IAG to find out how they compare with Air France-KLM. We also take a deep-dive into Latin America to explore the fortunes of Latam Airlines. Listen to the episode here, and find a full archive of the Lounge here.

Weekly Skies

Transatlantic Bliss, Gains in Spain

- IAG’s scorching hot performance this past summer cooled somewhat in the fourth quarter. Recall that in Q3, the company and all its constituent airlines improved their operating margins—versus both Q4 of 2022 and Q4 of 2019. Make no mistake, IAG followed with another good quarter from October to December. It just wasn’t as good, even adjusting for seasonality (Q4s are always much slower than Q3s). Operating margin was 7%, down from 8% in the same quarter a year earlier, and down from 12% in the same quarter of 2019. In any case, IAG finished 2023 with a formidable 12% full-year operating margin.

- The year stood out for strong transatlantic demand, which is IAG’s bread and butter. Premium demand was notably strong. So was leisure demand. So was premium leisure. And while margins at British Airways have slipped significantly from 2019, owing in part to operational headaches at London Heathrow, IAG’s Spanish airlines excelled, led by Iberia and Vueling (the post-pandemic tourism boom is greatly helping Spain’s economy). Iberia made clear that it wasn’t just the North Atlantic that thrived last year but also the South Atlantic (in other words, routes connecting Europe with Latin America). Iberia was IAG’s most profitable operation last year, with a 14% operating margin (its new A350s are extremely helpful, especially relative to the gas-guzzling four-engined A340s it previously flew). Aer Lingus was next with 12%, though it slipped to a small loss in Q4. BA and Vueling each posted a 10% figure, while the group’s loyalty program contributed handsomely; its margin was 22%.

- IAG also runs some smaller operations such as BA EuroFlyer from London Gatwick, BA CityFlyer from, you guessed it, London City, Iberia Express from Madrid, and Level from Barcelona. Level will soon have its own operating certificate, at which point IAG might deploy it on short-haul routes. IAG deftly (some might choose the adjective ruthlessly) uses its different operations as leverage against unions, allocating aircraft to units with the most favorable economics. It’s currently seeking new pilot deals with Aer Lingus and Vueling. The Aer Lingus talks, specifically, have hit a stalemate.

- Regarding corporate demand, IAG said traffic volumes are improving but remain well below 2019 levels. Measured by revenues, the decline is less but still substantial. Exact declines naturally vary by airline, with Iberia for one pretty much back to 2019 corporate revenue levels. Mitigating corporate revenue declines, in any case, are sharp gains in revenue from premium leisure travelers.

- Separately, IAG talked about driving more synergies between BA Holidays and the loyalty program. It talked about BA’s new B777-9s that will eventually arrive. A321-XLRs are coming too. And it said bookings for the critical North Atlantic market continue to look good into the upcoming second and third quarters.

- Looking ahead, IAG plans to double down on the Spanish–and the South Atlantic market–by taking full ownership control of Iberia’s rival Air Europa. But will regulators allow it?

Always an Adventure!

- As usual, Air France-KLM was a significantly less profitable company than its rival IAG last year. The Franco-Dutch giant was essentially half as profitable, earning just a 6% operating margin in 2023, compared to IAG’s 12%. During the fourth quarter of the year, Air France-KLM’s operating results dipped into the red, finishing with a negative 1% operating margin. KLM, historically the group’s profit champion, recorded lower margins than Air France in all but the third quarter last year. In Q4, KLM’s loss margins were slightly worse. One final point of comparison between the two airlines: Air France is now producing better margins than it was in 2019, thanks to major network, fleet, and other reforms. The opposite is true for KLM, wounded by hostile government policies.

- One big difference between IAG and Air France-KLM is the contributions of their respective low-cost units. Whereas Vueling thrived last year, Transavia posted losses, ending 2023 with a negative 4% operating margin. It’s a highly seasonal airline with heavy losses in Q4. But it’s also an airline undergoing a major overhaul–changes that management ultimately hopes will improve profitability. Most importantly, Air France is substituting mainline domestic flights for Transavia intra-European flights from slot-constrained Paris Orly airport. Domestic losses in France have long been a drag on company results. At the same time, Transavia is now introducing A320-family Neos and getting more aggressive with its ancillary sales.

- The group was significantly impacted by market disruptions last quarter. An earthquake in Morocco, war in Israel, and tourists spooked from Egypt and Jordan were problematic. Ditto for political unrest in Niger, Mali, and Burkina Faso, three large and profitable markets for Air France. In fact, the airline was unable to even fly over parts of western and central Africa, leading to re-routed services that increased fuel consumption.

- Disruptions notwithstanding, overall demand was strong in 2023. And it remains strong looking out into the next few months of 2024. “Actually the problem is not selling the tickets. We can sell every seat we want. It’s especially the difficulty to produce the tickets or the seats.” It’s referring there to aircraft delivery delays and other supply-side disruptions, which it said were currently affecting KLM more than Air France. Geographically, North America is booming. And while Air France-KLM has a large North American network, it doesn’t have as much relative exposure there as IAG. That’s true for South America too, where yields right now are “amazing.” India is another market where Air France and KLM are doing well thanks to additional business since Russia’s airspace closure forced a lot of capacity out of the market. Executives also mentioned strength in Bangkok and Singapore. East Asia overall, however, is not nearly what it was pre-pandemic, with China and Japan still down sharply in terms of capacity.

- Consistent with pretty much what every other airline in the world is saying, premium leisure demand on most routes is red hot. In Paris specifically, it’s “very, very strong.” As for corporate demand, it’s down for Air France-KLM. But management reminded investors that cities like Paris and Amsterdam aren’t as dependent on corporate traffic as London.

- Besides Transavia’s new Neos, Air France and KLM are betting big on the A350. Air France is also using A220s, while KLM swaps B737-NGs for Neos. For the record, it’s buying CFM engines for its NEOs, not Pratt GTF engines. It does use GTFs on its A220s, however.

- Air France-KLM naturally wants to squeeze more profits from its Flying Blue loyalty plan. It also owns a profitable maintenance business. It’s more exposed to cargo than IAG, which was helpful during the pandemic but less so now. Still, cargo yields are higher than they were in 2019.

- It will be an even busier summer than normal this year, with Paris hosting the summer Olympics and Paralympics. But the event isn’t likely to do much for profits. Many business travelers will stay away during the games. And traffic flows will be highly directional, with planes flying out of Paris pretty empty at the start of the games, and into Paris empty towards the end.

- What’s the latest on Air France-KLM’s consolidation plans? It’s now got SAS firmly within its sphere of influence, holding a 19% ownership stake in the bankrupt Scandinavian carrier. SAS is already moving flights to Atlanta, for synergies with Air France-KLM’s joint venture partner Delta. Virgin Atlantic is part of that JV as well. Eventually, the idea is for SAS to join the JV, but that requires antitrust immunity from regulators. Air France-KLM, remember, retains an option to buy full control of SAS.

- In the meantime, TAP Air Portugal remains on its radar. “As you know,” said Air France-KLM’s CEO Ben Smith, “geographically, we’re quite interested in that operation.” But Portugal’s intentions on whether to sell TAP are still unclear. Smith and his team are surely keeping an eye on Air Europa as well, in the event IAG’s takeover plans are torpedoed by regulators.

- We’ll close with a fun fact from Air France-KLM: It claims to be the world’s largest user of sustainable aviation fuels. And a fun quote from Ben Smith: “Running a business in our industry is always an adventure.”

Volaris: A Year of Many Headaches

- It’s hard to say anything negative about an 18% operating margin. But things weren’t quite as good as it sounds for Volaris in the fourth quarter of 2023. That 18% figure includes an unspecified boost from compensation the airline negotiated with Pratt & Whitney. Yes, Volaris is yet another GTF victim, dealing with disruptions from Airbus Neos being taken out of service for inspection for about a year.

- The normally fast-growing LCC, which depends on growth to control unit costs, wound up flying 1% fewer ASMs last quarter than in the same quarter a year earlier. The sudden Neo removals, furthermore, forced Volaris to re-accommodate early-booking leisure and family-visit customers onto seats it was hoping to reserve for higher-yielding late-booking customers. The GTF inspections, alas, are expected to extend into 2026.

- Another headache constraining growth: slot restrictions at Mexico City’s main airport. On the other hand, Mexico’s airlines finally received FAA clearance to expand their U.S. flying, prompting Volaris to grow international ASMs by 22%, even as domestic ASMs dropped 11% (domestic still accounted for 62% of the total). An ancillary benefit of more U.S. flying is more U.S. dollar-denominated revenue, which lowers forex risk. And speaking of ancillary benefits, ancillaries (non-ticket sales) crossed the 50% threshold for the first time. Keep this fact in mind when considering the airline’s upgauging strategy: It wants large 200-plus seat narrowbodies because it can fill extra seats with passengers paying very low fares and still make money from them by selling ancillary items. It’s the kind of thinking adopted by many LCCs, helping to explain the immense popularity of the A321-Neo.

- Of course, Volaris isn’t alone when it comes to aircraft disruptions. Mexico is essentially a three-airline market, and rivals VivaAerobus (also a GTF customer) and Aeromexico (a Max customer) have their own issues. The resulting shortage of capacity is creating a revenue tide that’s lifting all boats, at least partly offsetting the negative impact on unit costs. And no, the new government-run reboot of Mexicana is a non-factor, thus far anyway.

- Volaris did highlight its labor cost advantage versus U.S. rivals, having increased its wages just 5% this month. “All other costs remain controlled, with lower ASMs expected to be the primary constraint on cost performance this year.” Compare this to Southwest, for one, which just handed its mechanics an 18% wage hike (albeit after three years without any hikes).

- Demand is fine, even in beach markets where U.S. carriers have cited overcapacity—Volaris flies mostly Mexican tourists (not American tourists) to destinations like Cancun. Elsewhere, capacity growth will ease from its bases in Central America (Costa Rica and El Salvador). On U.S. markets, it’s ramping up cooperation with Frontier, also owned by Bill Franke’s Indigo Partners, an airline investment firm.

- Looking back at 2023, it was a year that Volaris would probably want to forget. It wound up finishing the year with a respectable 6% operating margin after losing money in the first three quarters. But again, the compensation from Pratt was a big part of that. Management, nevertheless, was quick to explain that the Pratt compensation does not fully account for lost revenues, just the associated fixed costs tied to dealing with the removals from service.

U.S. Airlines Face New Wheelchair Rules

- The U.S. Department of Transportation has proposed tough new rules on how airlines should accommodate passengers who use wheelchairs. Transportation Secretary Pete Buttigieg described the plans as the largest expansion in passenger rights for those with wheelchairs since 2008.

- Under the proposals, delaying the return of a wheelchair or mishandling it would become an automatic violation of a federal law that prohibits airlines from discriminating against passengers with disabilities, making it easier for the DOT to penalize airlines. The plan would also require airlines to provide a temporary replacement wheelchair to affected travelers. Companies would have to promptly fix any damaged items, while also covering the cost of repair. Passengers with wheelchairs will have the right to choose a vendor for any repairs or replacements, and airlines would have to cover those costs, too.

- Airlines would be required to return any delayed wheelchairs to a passenger’s final destination within 24 hours and provide wheelchairs as close as possible to the aircraft door for exiting passengers. The new proposals would also mandate annual hands-on training for airline employees and contractors who assist travelers.

— Jay Shabat and Gordon Smith

Fleet

Max Pain for Ryanair

- Ryanair will receive 30% fewer new planes than expected ahead of the all-important summer season. Michael O’Leary, the chief executive of Ryanair, said he is “very disappointed” with additional delays to deliveries of Boeing 737 Max jets. The Irish budget airline group is one of Boeing’s biggest customers. It operates a fleet comprised almost entirely of 737-800 and 737 Max aircraft.

- In a statement published on Friday, it confirmed that only 40 new planes due for delivery before July will arrive on time. While 57 aircraft were originally expected, Ryanair said it had already baked in some flexibility to its flying program. The summer schedule currently on sale was based on receiving at least 50 of the 57 new aircraft. To compensate for the further shortfall of 10 units, the carrier is making further cuts to some flights. It said this would take the form of reducing frequencies on existing services rather than axing new routes entirely.

- Removing 17 planes from a fleet of 600 aircraft may seem modest, but context is key. The new deliveries are for an optimized version which Ryanair calls the Boeing 737-MAX8200. Along with 16% lower fuel costs, these jets can carry up to 197 passengers – more than the 189 on Ryanair’s older planes.

- While Ryanair is usually profitable year-round, it is during the summer that it really makes its money. With almost every seat occupied at peak holiday-time pricing, the delivery deficit will hit the bottom line harder than a winter delay. Ryanair said the changes will reduce its traffic for the 2024-25 financial year from 205 million to between 198 and 200 million. This would still be a net increase on the previous year, but lower than hoped. The airline is selecting “higher cost airports” to make the schedule cuts. It singled out Milan Malpensa, Dublin, Warsaw Modlin, and four Portuguese cities as places where service reductions will be made. All affected passengers will be offered alternative flights or full refunds.

- Despite this latest setback, Ryanair Group CEO, Michael O’Leary, delivered another strong endorsement of the beleaguered plane maker. “Boeing continues to have Ryanair’s wholehearted support as they work through these temporary challenges, and we are confident that their senior management team, led by Dave Calhoun [CEO] and Brian West [CFO], will resolve these production delays and quality control issues in both Wichita and Seattle,” said O’Leary. “We are working with our airport partners to deliver some growth to them, albeit later in September and October, rather than July and August. This traffic growth can only be delivered at lower fares during these shoulder months.”

Thoughts from the World’s Largest Aircraft Lessor

- AerCap CEO Aengus Kelly, fielding analyst questions during the company’s latest earnings call, addressed the specifics of today’s narrowbody market. Airbus is clearly outselling Boeing when it comes to single-aisle planes, “and has been for some time.” But it’s all because of one specific model: the A321-Neo. The smaller A320-Neo, by contrast, hasn’t been selling nearly as well. In that size category, Boeing is winning with its B737-Max 8 (it offers a modestly larger Max-9 as well, though without too much interest).

- One question is whether the Max 10 can compete effectively with the A321-Neo. Kelly is doubtful. “The Max 10 has not yet been certified, and it’s not as capable an airplane.” [the range, for one, is less, and there’s only one engine source available]. Kelly says AerCap is “very bullish on the Max 8,” which is in high demand among airlines, and also in short supply currently. (AerCap has 120 Maxs on order). “But because of the A321 superiority over the larger Boeing product, and the fact that it’s so early to the market versus the Boeing product, we are going to see a significant majority of that market heading towards the Airbus product line for the long term.”

- Kelly was separately asked about the A220, and whether Airbus might produce a larger -500 version to go along with its -100s and -300s. “Listen,” he said, “I think the manufacturers should focus on making what they have… they should focus on their customers now and delivering the promises as they have made and delivering them on-spec, on-time.”

FAA Gives Boeing 90 Days

- Boeing has 90 days to develop a plan to address its quality control issues following a history of problems with its 737 Max program, Federal Aviation Administration chief Michael Whitaker has said. His remarks follow an all-day safety discussion that the federal agency had with Boeing at its headquarters last week. Whitaker told the plane maker he expects the plan to take into account the latest results from the FAA’s audit of its production processes and the findings from a recent expert panel report.

- Boeing CEO Dave Calhoun said the company’s leadership team is “totally committed to meeting this challenge.” “By virtue of our quality stand-downs, the FAA audit findings, and the recent expert review panel report, we have a clear picture of what needs to be done,” Calhoun said. “Transparency prevailed in all of these discussions.”

— Jay Shabat and Gordon Smith

Routes and Networks

Flying Norse to Nigeria

- Norwegian low-cost airline Norse Atlantic Airways is heading for Nigeria. The addition of the West African nation is unusual for the carrier, which usually flies from Europe to the United States and the Caribbean. The new service will link Lagos to London and operate as a charter for Nigerian airline Air Peace. The ACMI contract provides the airplane, crew, maintenance, and insurance to the charter client. The move has been described by Norse as marking “the beginning of a strategic partnership” between the two companies.

- The new Nigeria flights are due to begin in April and will initially run for two months. Charters will operate four-times weekly from London’s Gatwick Airport. The parties say there is potential for a longer-term agreement, however, it is unclear if or how this will be decided. Although Norse is already a major operator at Gatwick, it will be using new slots allocated to Air Peace for the route. The development will put the Nigerian carrier in competition with British Airways and Virgin Atlantic, who already operate from London Heathrow to Lagos. For its part, the Lagos-London link will mark Air Peace’s first foray into the European market. The airline currently flies within Africa as well as select routes to the UAE, China, and India.

- Separately, Norse Atlantic reported deeply red financial results last week, covering the fourth quarter of 2023. Its operating margin was (ouch) negative 60%. The airline secured impressively low lease rates on its 15 B787s, but those rates won’t last forever. Management does say that demand is strong. In the meantime, Norse is working with consultants to perhaps sell a stake in itself to another airline. It did make a bit of money during last year’s peak summer season. But it will need to do better to ensure survival.

Tapping into the Americas

- TAP Air Portugal is ramping up summer season services to the Americas. For Brazil, there will be an additional six flights a week between Lisbon and Recife, with an extra two flights a week to both Fortaleza and Rio de Janeiro. Other enhancements will be made to Belém, Brasília, Natal/Maceio, Porto Alegre, Salvador, and São Paulo. This will give TAP a total of 96 flights a week between Portugal and Brazil this summer, compared to 80 during the same period in 2023.

- As for the United States, TAP is operating 77 flights a week this summer, five more than last year. There will also be 20 weekly flights to Canada, five more than in 2023. In other developments, the company will fly thrice-weekly between Lisbon and Caracas in Venezuela. One of these three services is particularly notable as it will stop at Funchal on the island of Madeira on the inbound sector.

Qatar Resumes Osaka Kansai

- Qatar Airways has enhanced its Japanese network with the addition of Osaka. The route was restarted on March 1 and represents only its second destination in Japan after Tokyo. The nonstop daily services from Doha to Kansai International are operated by Airbus A350-900s.

- The jets, which are equipped with 36 seats in business class and 247 in economy, were previously at the center of a high-profile dispute between the airline and Airbus. Qatar Airways alleged surface degradation issues with its planes, resulting in a grounding of the widebody airliner. In February 2023, the two parties announced they had reached an “amicable and mutually agreeable settlement.” enabling the fleet to get back in the air.

- The economics of the Osaka route are boosted by Qatar’s codeshare partnership with oneworld partner Japan Airlines. This allows Qatar passengers to connect onwards to 34 destinations across Japan. The Japanese flag carrier also places its code on all Qatar flights between Doha and Japan.

Route Round-Ups

- Aeromexico is bolstering its presence in the Sunshine State. On July 1, the flag carrier will launch a daily nonstop service linking Mexico City International with Tampa. It’ll be operated by an Embraer 190 with 99 seats; 11 in premium and 88 in economy. Tampa will be the company’s 23rd U.S. destination and continues a period of major route development for Aeromexico.

- Emirates is building back more of its pre-pandemic network. From May 1, the Dubai-based giant will return to Cambodia. The airline will offer a daily fifth-freedom flight via Singapore to Phnom Penh using a three-class Boeing 777-300ER.

- Etihad Airways is adding two new destinations to its route map. From June 15, it will begin a thrice-weekly seasonal service from Abu Dhabi to the Turkish resort of Antalya. The following day, on June 16, operations to Jaipur will start with four weekly rotations. The new link will represent Etihad’s 11th Indian destination.

State of the Unions

Turbulence Eases at Transat

- A majority of flight attendants at Air Transat have voted in favor of a new terms and conditions deal. Of those balloted, 62.7% agreed to accept the recommendation of the Federal Mediation and Conciliation Service.

- The move lifts the strike threat that has been hanging over the Canadian leisure carrier as it enters the summer season. The collective agreement is backdated to November 1, 2022, and is valid until October 31, 2027. Julie Lamontagne, Chief People, Communications and Sustainability Officer of Transat said the result had followed “an unprecedented process.”

- For its part, the Canadian Union of Public Employees (CUPE) said the new deal, which gives total compound salary increases of 30% over five years, will make Air Transat crews the highest paid in the country. The airline has around 2,100 flight attendants.

- Alongside pay rises, the agreement secures the number of crew seats on all flights lasting seven hours or more and those departing Canada after 10 pm. It also increases the number of personal leave days and vacation days. Chantal Bourgeois, CUPE National Representative, described the process as “long and complex”. She added: “This will be an extremely well-deserved adjustment after years of effort to help the company through financial difficulties, followed by the catastrophic years of the pandemic and a period of high inflation.”

Feature Story: The South American Airline Paradox

An aviation hellscape? Or an aviation paradise? Sometimes, it’s hard to tell which.

At first glance, South America’s post-pandemic airline industry looks like a junkyard of bankrupt companies. Latam: bankrupt in 2020. Avianca: also bankrupt in 2020. Gol: bankrupt in 2024. Azul: Narrowly avoided bankruptcy in 2023. The reality, however, is different. It’s not a junkyard. It’s a collection of gems.

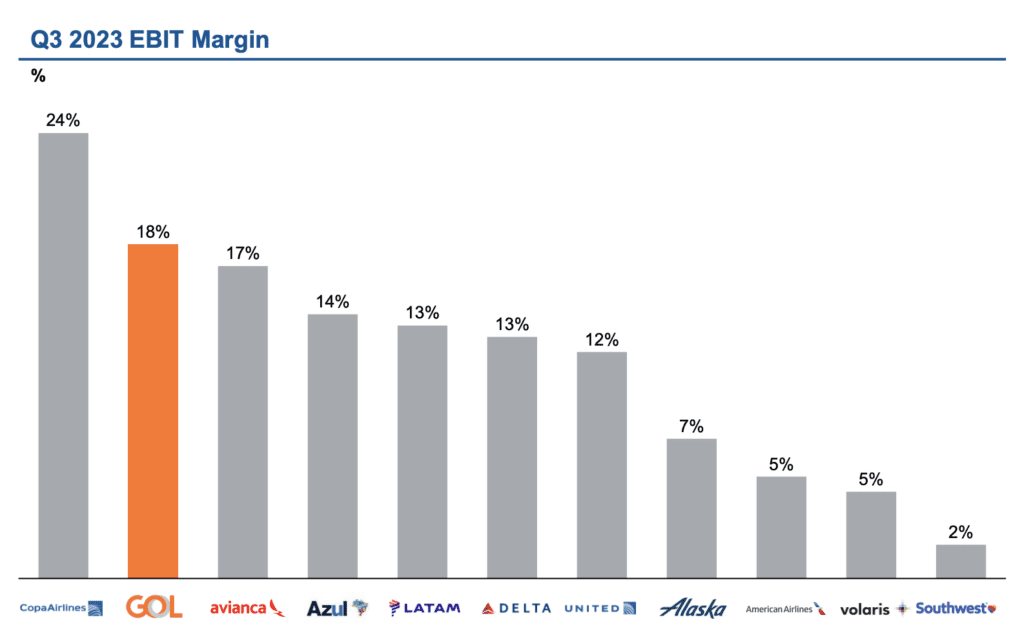

Today, these four airlines are among the world’s most profitable, reporting double-digit operating margins throughout 2023. As 2024 progresses, South America’s Big Four find themselves dominating the continent’s airline market, needled here and there by nascent low-cost carriers but otherwise competing mostly with each other.

The paradox of South America’s Big Four was on display again last month, when Gol filed for bankruptcy shortly after reporting an outstanding 18% operating margin for the July-to-September quarter (an off-peak period in South America). Huh? Azul did even better in Q3. But still, it was at the precipice of bankruptcy, narrowly avoiding it with a voluntary restructuring of its obligations, to lenders, lessors, and other creditors. How does this make any sense?

As benign as conditions are today, South America’s airlines received almost no material financial support from their governments during the Covid crisis. The crisis inevitably scarred their balance sheets, leaving debts they struggled to pay. Making matters worse, severe currency depreciation ballooned the cost of debt they owed in U.S. dollars. In 2019, for example, the Brazilian real was worth roughly 25 U.S. cents. It’s now worth only 20. Multiply that across billions of dollars, and it’s no wonder why carriers like Gol and Azul were having so much trouble meeting their obligations, even as their businesses produced solid profits and operating cash flows.

Latam, which was the first among South America’s Big Four to file, exited court protection in late 2022. It’s now performing better than it was before its bankruptcy—the latest manifestation is a $132m net profit for the October-to-December quarter of 2023. Its operating margin was 11%, which is also what it earned for the entire year.

In its Q4 earnings call, Latam’s management cited many of the reasons why it’s currently faring so well. One is its “extremely competitive fleet costs,” achieved thanks to contract renegotiations during the depths of the Covid downturn, when lessors had few options to redeploy their planes. Latam, in other words, went through bankruptcy at an opportune time. (As Gol is finding out, lessors are far less willing to offer concessions today). Many of the fleet contracts Latam renegotiated, importantly, won’t expire until late this decade. This implies a competitive cost advantage locked in for several more years to come.

Overall Latam’s passenger business got its nonfuel unit costs down to just over four U.S. cents a kilometer. That’s even a bit lower than what it was in 2019, despite higher labor and maintenance costs. A cost structure so low makes it difficult for would-be LCC challengers, especially on routes within South America. There, Latam essentially operates like an LCC. It flies single-class densified narrowbodies, distributes largely online, charges for bags and other ancillaries, etc. Overall, Latam says it slashed $1.3b from its cost structure during bankruptcy. That’s a sharp contrast to most carriers elsewhere in the world, which have spent the past few years battling heavy cost inflation.

Latam also counts its loyalty program, now with 45 million members, as a key competitive weapon. Its large cargo operation saw revenues slip from pandemic-era highs, but cargo yields remain well above 2019 levels. In a bold move just before the pandemic, Latam dumped American and partnered with Delta, following Chile’s refusal to allow a Latam-American joint venture. By 2022, it had all the approvals it needed for a full, antitrust-immune alliance with Delta, which is just now starting to pay dividends. The two airlines have introduced new routes at a rapid clip, with Latam itself adding Sao Paulo-Los Angeles, Medellin-Miami, Bogota-Orlando, and Lima-Atlanta. Delta added Atlanta-Cartagena and New York JFK-Rio de Janeiro. Delta, importantly, retained a 10% ownership stake in Latam following the latter’s bankruptcy. Qatar Airways, for the record, owns another 10%.

“Today, we are the owners of our own destiny in the region,” said Latam CEO Robert Alvo. “We’re very proud of what we’ve done.” Alvo and his team say bookings continue to look strong. Latam is actively looking to add more planes, even B737 Maxs if available from Gol or whomever. For now, it is flying Airbus narrowbodies, including A321-Neos for upgauging. On the widebody side, its aircraft of choice is the B787, having abandoned its A350s. It also flies B777s and B767s. Will it buy the new B777X? Alvo hinted that Boeing’s new widebody might be too large for Latam’s needs. “Our flows are not very big.”

One can’t explain Latam’s strong operating profits—nor those of Gol and Azul—without recognizing the current strength of the Brazilian market. The country accounts for roughly half of South America’s population, supporting by far its largest airline market. Brazil is the seventh most populous country in the world, and—according to Cirium Diio schedules for 2023—its seventh largest airline market (just behind Spain and ahead of Germany). But Brazil only has three airlines of national significance—indeed, Latam, Gol, and Azul.

Until 2019, it had a fourth: Oceanair, which was branded Avianca Brasil. But Avianca Brasil collapsed, leaving lots of pricing power for the incumbents. As Latam explained, “We certainly are seeing a different industry in Latin America than pre-pandemic. We have seen certain operators that are no longer operating in certain markets. There was a little bit of consolidation. So, the competitive environment is different and therefore, a little bit more stable and a little bit more balanced.” It also noted how capacity will be constrained in the years ahead due to aircraft production and engine issues.

Avianca too, watched with glee as a key domestic rival collapsed, in this case Viva Air, which stopped flying around this time last year. Latam’s Colombian affiliate was the other big beneficiary of Viva’s demise. Like Latam, Avianca emerged from bankruptcy (in late 2021) with an LCC-like cost structure, to supplement a profitable loyalty plan and cargo business. It’s now flying more short-haul point-to-point routes with planes flying nearly two additional hours per day compared to 2019. Its passenger fleet is simple: Just Airbus A320-family planes and B787-8s. Like Gol and Azul, Avianca will report its Q4 results later this month.

And yes, there are other airlines in South America. JetSmart, an LCC with ownership links to Wizz Air, Frontier, and Volaris, is a low-cost carrier flying throughout the continent. So is Chile’s Sky Airline. Both are relatively small. State-owned carriers like Aerolineas Argentinas and Boliviana, never mind Conviasa, are… let’s be nice and call them competitively challenged. (Aerolineas is performing somewhat better these days but remains an industry metaphor for ineptitude). Of course, strong carriers from outside the region—like Copa, American, Iberia, and TAP—are more formidable competitors on overseas routes. Overall, however, it’s a rather benign competitive environment for South America’s Big Four.

Or should we call them South America’s Big Three? Last year, Avianca and Gol merged, further mitigating competitive pressures. As it happens, the international market within South America is surprisingly small, with Avianca, Gol, and Latam currently offering just five flights a day, for example, between the giant cities of Bogota and Sao Paulo. There are just one or two daily flights (depending on the day) that run between Bogota and Rio de Janeiro. With the vast Amazon rainforest and Andes mountain range taking up so much of the continent’s land mass, intercity commercial links have historically been slow to develop across borders. The distances are vast too—Bogota-Sao Paulo is longer than New York-Los Angeles!

The Avianca-Gol merger will not, therefore, have a dramatic impact on South America’s competitive dynamics; there’s almost no overlap between the two carriers. They’ll remain separately branded too, with separate financials under the umbrella of a holding company called Abra. Currently, it is helping to fund Gol’s flying while in bankruptcy. At one point during the pandemic, Azul expressed interest in merging with Latam. A deal that would have left just two surviving Brazilian domestic players, however, would surely have triggered antitrust resistance.

As things stand now, 2024 is shaping up to be another strong year. Latam, for its part, expects to earn an operating margin of somewhere between 11% and 14%. That’s even as it grows international ASK capacity to a targeted 17%. The airline feels confident enough to grow cargo capacity by double-digits this year as well. An airline hellscape? Sure doesn’t sound like one.